![[object Object] icon](/_next/static/media/home.59b745c9.svg)

![[object Object] icon](/_next/static/media/buy.57cae078.svg)

![[object Object] icon](/_next/static/media/rent.2864d22a.svg)

![[object Object] icon](/_next/static/media/commercial.5f5f9bbc.svg)

![[object Object] icon](/_next/static/media/condos.8a55189e.svg)

![[object Object] icon](/_next/static/media/newLaunches.e1f1ccfd.svg)

![[object Object] icon](/_next/static/media/agents.9f8252e2.svg)

![[object Object] icon](/_next/static/media/guides.f567fc08.svg)

![[object Object] icon](/_next/static/media/contactUs.a39ef3b7.svg)

![[object Object] icon](/_next/static/media/aboutUs.e47cbd6d.svg)

)

Shariah-Compliant Home Financing: The Global Shift Toward Ethical Homeownership

Key Takeaways

- Ethical Financing Growth: Shariah-compliant home financing is expanding rapidly beyond traditional markets.

- Interest-Free Structures: Islamic mortgages avoid interest by using trade, leasing, or partnership models.

- Trust and Transparency: Buyers prioritize clarity, fairness, and strict compliance when choosing financing options.

- Global Expansion: Islamic finance is gaining traction in Western countries and non-Muslim markets.

- Ongoing Challenges: Issues like compliance authenticity and governance remain key concerns.

Introduction: A New Era of Ethical Homeownership

In 2026, Shariah-compliant home financing is no longer a niche topic—it’s one of the fastest-growing conversations in global finance. From Southeast Asia to North America, more homebuyers are asking a simple question: can I own a home without compromising my beliefs?

Driven by rising demand, stricter ethical expectations, and new financial innovation, Islamic home financing is undergoing a major transformation. This shift reflects a broader movement toward trust, transparency, and fairness in how people buy homes.

What Is Shariah-Compliant Home Financing?

At its core, Shariah-compliant home financing follows Islamic law, which prohibits riba (interest) and promotes ethical financial dealings. Instead of traditional borrowing, financial institutions structure transactions around trade, leasing, or partnerships, ensuring compliance with religious principles1.

In practical terms, this means the bank purchases the property and then sells or leases it to the buyer at a profit, with payments structured in a transparent and agreed manner. This model forms the backbone of modern Islamic finance solutions and continues to evolve with fintech integration2.

How Islamic Mortgages Work in Practice

In countries like Malaysia, Islamic home financing is highly developed, with banks offering structured products tailored to modern buyers. These include cost-plus-profit arrangements and flexible financing models that align with Shariah requirements3.

Financial institutions are also innovating to provide adaptable solutions that meet customer needs while maintaining compliance, showing how Islamic finance is evolving alongside conventional systems4.

International banks have also entered the market, integrating Shariah-compliant offerings into their portfolios, reinforcing the idea that Islamic financing is becoming a mainstream option globally5.

Why Demand Is Rising

The growing popularity of Shariah-compliant home financing is driven by more than religious considerations. Ethical finance is gaining traction among a broader audience that values fairness, shared risk, and accountability in financial transactions.

Research indicates that transparency, trust, and strict adherence to compliance standards are among the most influential factors for consumers choosing Islamic home financing options6.

At the same time, a younger and more informed generation of buyers is demanding clarity and flexibility, pushing institutions to innovate faster and offer more transparent solutions7.

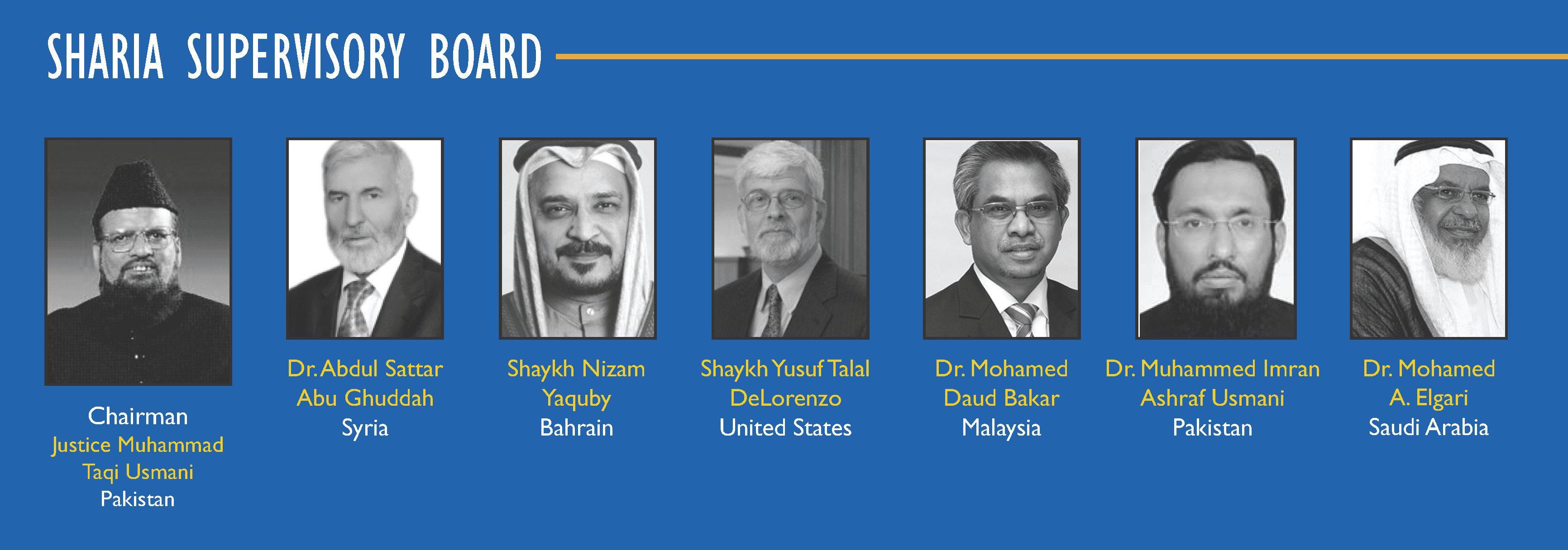

The Role of Shariah Boards: Guardians of Compliance

Governance plays a crucial role in ensuring that Islamic home financing remains authentic and trustworthy. Every product must be reviewed and approved by a Shariah Board, which ensures that financial structures comply with Islamic principles and ethical standards8.

{kind=link}

)

Scholarly oversight and governance frameworks supporting ethical financial compliance

These boards are responsible for approving structures, monitoring ongoing compliance, and maintaining the integrity of financial products, making them essential to the credibility of the entire system.

Challenges: Is It Truly Shariah-Compliant?

Despite its growth, the industry faces increasing scrutiny. Concerns have been raised about whether all products fully adhere to the spirit of Shariah, especially in leading markets where reform and improved transparency are being discussed9.

Additional academic discussions highlight the need for stronger governance and clearer frameworks to ensure that compliance is not only technical but also ethical in practice10.

One major issue is Shariah Non-compliance Income (SNCI), particularly in certain financing structures, which can affect trust and raise ethical concerns within the industry11.

Global Expansion: Beyond Muslim-Majority Markets

Islamic home financing is increasingly expanding into global markets. In Singapore, the introduction of Shariah-compliant home financing reflects growing acceptance even within conventional financial systems12.

Meanwhile, in Canada, innovative startups are making Islamic mortgages accessible to minority communities, offering transparent and ethical alternatives to traditional interest-based loans13.

This global expansion highlights how Islamic finance is no longer geographically limited but is becoming increasingly relevant worldwide14.

{kind=link}

What Homebuyers Should Look For

Choosing the right Shariah-compliant home financing product requires careful evaluation. Buyers should prioritize transparency, ensuring they fully understand how the financing works and how profits are structured.

- Transparency: Clear breakdown of costs and payment structures.

- Authenticity: Alignment with both the letter and spirit of Shariah.

- Shariah Board Oversight: Verified supervision by qualified scholars.

- Flexibility: Features such as early settlement and competitive pricing.

The Future of Shariah-Compliant Home Financing

The future of this sector will likely be shaped by increased standardization, stronger regulation, and continued innovation. As fintech continues to evolve, Islamic financing solutions are expected to become more accessible, transparent, and efficient15.

At the same time, the appeal of ethical finance is expected to broaden, attracting a wider audience beyond traditional markets and reinforcing the global relevance of Shariah-compliant solutions.

Final Thoughts

Shariah-compliant home financing in 2026 stands at a critical intersection of growth and scrutiny. While expansion and innovation are opening new opportunities, maintaining trust and authenticity remains essential.

Ultimately, its success will depend on balancing ethical principles with modern financial needs, creating a system that is transparent, fair, and aligned with the values of diverse homebuyers.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional mortgages?

Answer: Shariah-compliant financing avoids interest and instead uses trade-based or partnership models where the bank buys and sells or leases the property to the buyer.

Question: Is Islamic home financing only for Muslims?

Answer: No, it is open to anyone interested in ethical, transparent financial products, including non-Muslims seeking alternatives to interest-based loans.

Question: Are all Islamic financing products truly compliant?

Answer: Not always, which is why buyers should check for proper Shariah Board oversight and ensure the product follows both the technical and ethical principles of Islamic finance.

Disclaimer: The information is provided for general information only. JYMS Properties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.