![[object Object] icon](/_next/static/media/home.59b745c9.svg)

![[object Object] icon](/_next/static/media/buy.57cae078.svg)

![[object Object] icon](/_next/static/media/rent.2864d22a.svg)

![[object Object] icon](/_next/static/media/commercial.5f5f9bbc.svg)

![[object Object] icon](/_next/static/media/condos.8a55189e.svg)

![[object Object] icon](/_next/static/media/newLaunches.e1f1ccfd.svg)

![[object Object] icon](/_next/static/media/agents.9f8252e2.svg)

![[object Object] icon](/_next/static/media/guides.f567fc08.svg)

![[object Object] icon](/_next/static/media/contactUs.a39ef3b7.svg)

![[object Object] icon](/_next/static/media/aboutUs.e47cbd6d.svg)

)

Shariah-compliant home financing: A 2026 guide to ethical homeownership

Key Takeaways

- Interest-Free Structure: Financing avoids riba and replaces it with profit-based transactions.

- Asset-Backed Approach: Every transaction is tied to real assets rather than pure lending.

- Growing Popularity: Increasing demand for ethical finance is driving adoption globally.

- Risk Sharing: Financial responsibility is structured more fairly between bank and buyer.

- Modern Innovation: Banks are developing competitive and flexible Shariah-compliant products.

Introduction to Shariah-compliant home financing

Shariah-compliant home financing is quickly becoming one of the most talked-about trends in global property and finance. As more buyers look for ethical, transparent, and faith-aligned ways to own a home, this alternative to conventional mortgages is stepping into the spotlight1.

From Malaysia’s mature Islamic finance ecosystem to Singapore’s emerging offerings, the industry is evolving fast in 2026. But what exactly is Shariah-compliant home financing—and why is it gaining so much attention right now?

)

Modern residential developments reflecting ethical and sustainable homeownership trends

What is Shariah-compliant home financing?

At its core, Shariah-compliant home financing follows Islamic law (Shariah). Unlike traditional mortgages, it eliminates interest and focuses on fairness, shared responsibility, and real asset-backed transactions. Instead of lending money, banks structure deals through buying and selling arrangements2.

For example, a bank may purchase a property first and then sell it to the buyer at a profit, allowing repayment through installments. This ensures transparency and aligns the transaction with ethical financial principles.

How it actually works (in simple terms)

One of the most common structures used is Commodity Murabahah. In this model, the bank purchases a commodity, sells it to the buyer at a profit, and the buyer then converts it into cash to finance the home purchase. The process ensures that every step involves a tangible asset rather than pure lending3.

- The bank buys a commodity

- The commodity is sold to the buyer at a profit

- The buyer sells it for cash

- The cash is used to purchase the home

The principles behind Islamic home financing

Islamic finance is built on key principles such as risk sharing, asset-backed transactions, avoidance of uncertainty, and ethical dealings. These principles guide how every product is structured and ensure fairness in financial relationships4.

This approach appeals not only to Muslims but also to a broader audience seeking transparency and responsible financial systems.

Why Shariah-compliant home financing is trending in 2026

The growing demand for ethical finance is a major driver behind the rise of Shariah-compliant home financing. Buyers are increasingly aligning their financial decisions with their personal values, including fairness and sustainability.

At the same time, Southeast Asia continues to lead the way, with Malaysia offering a mature ecosystem and Singapore expanding its options in a multicultural environment5.

Major banks are also innovating rapidly, introducing flexible and competitive products that combine compliance with modern financial needs.

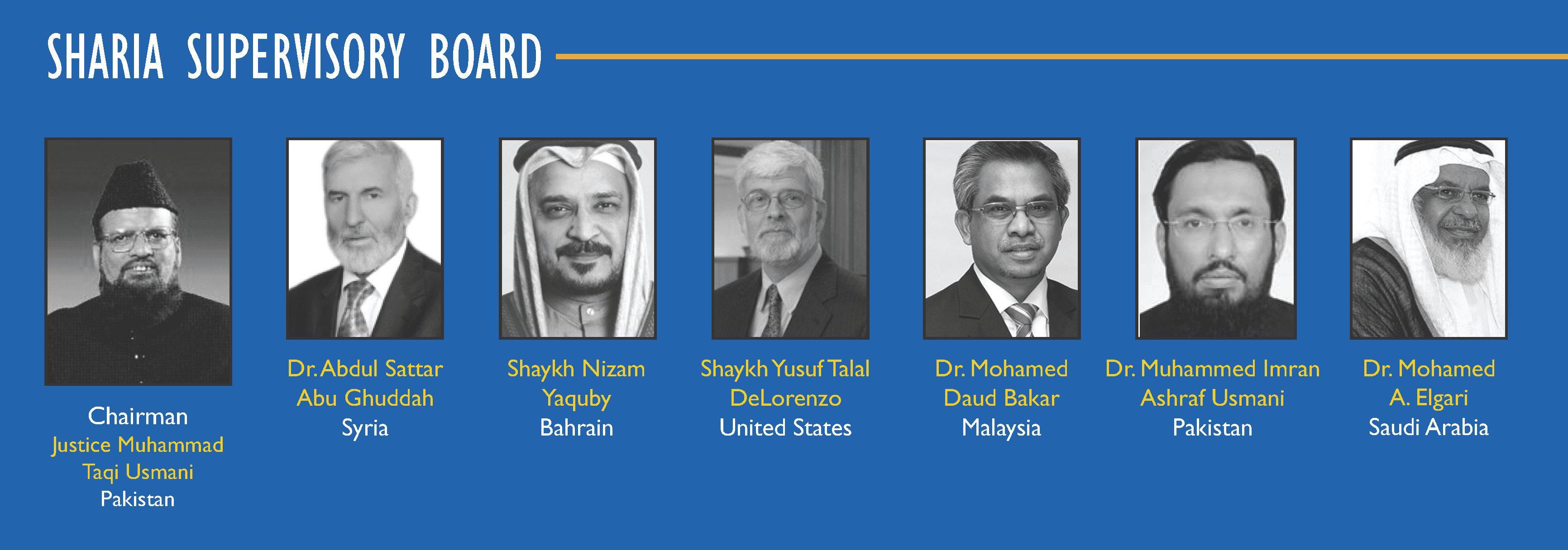

The role of the Shariah Board

The Shariah Board plays a critical role in ensuring that financial products comply with Islamic law. These scholars review structures, monitor transactions, and maintain ethical integrity throughout the financing process6.

{kind=link}

This governance framework builds trust and ensures that all transactions remain aligned with religious and ethical standards.

Challenges the industry still faces

Despite its growth, the industry faces several challenges. Concerns around transparency and authenticity have led to discussions about the need for reform and stronger compliance systems7.

Additionally, complex structures like tawarruq can make it difficult for consumers to fully understand the financing process, highlighting the importance of education and clarity.

There are also concerns about non-compliant income risks and the need for stronger verification mechanisms to maintain system integrity8.

What do consumers think?

Consumer perception plays a crucial role in adoption. Awareness, trust, and understanding of ethical benefits significantly influence whether buyers choose Islamic financing options9.

As education improves and products become easier to understand, adoption rates are expected to increase further.

Comparing Islamic vs conventional mortgages

Conventional mortgages are based on lending money with interest, placing most of the risk on the borrower. In contrast, Shariah-compliant financing involves structured transactions where profit replaces interest and risk is distributed more fairly.

While both lead to homeownership, the financial philosophy and execution differ significantly.

Is it more expensive?

Shariah-compliant home financing is not necessarily more expensive than conventional loans. Many banks price their products competitively to match market rates while maintaining compliance.

However, costs can vary depending on structure, bank policies, and market conditions, so comparing options remains essential.

The future of Shariah-compliant home financing

The future of this financing model looks promising, with trends pointing toward greater standardization, digital innovation, broader market adoption, and stronger governance frameworks.

These developments are expected to enhance transparency, simplify processes, and make ethical home financing more accessible globally.

What this means for homebuyers

For homebuyers in 2026, Shariah-compliant home financing offers a compelling alternative that aligns financial decisions with ethical values.

- Ethical financial practices

- Transparent transactions

- Faith-aligned investing

Understanding the structure and comparing available options are key steps before making a decision.

Final thoughts

Shariah-compliant home financing is no longer a niche concept. It is becoming a mainstream option driven by ethical demand, innovation, and strong regional leadership.

As the industry continues to evolve, maintaining transparency, trust, and true compliance will be essential for long-term success.

Frequently Asked Questions

Question: What makes Shariah-compliant financing different from conventional loans?

Answer: It avoids interest and instead uses asset-based transactions with profit structures, ensuring ethical and transparent financing.

Question: Is Shariah-compliant home financing only for Muslims?

Answer: No, it is open to anyone interested in ethical and transparent financial solutions, regardless of religion.

Question: Are these financing options harder to understand?

Answer: Some structures can be complex, but banks and institutions are improving clarity and education to make them more accessible.

Disclaimer: The information is provided for general information only. JYMS Properties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.