![[object Object] icon](/_next/static/media/home.59b745c9.svg)

![[object Object] icon](/_next/static/media/buy.57cae078.svg)

![[object Object] icon](/_next/static/media/rent.2864d22a.svg)

![[object Object] icon](/_next/static/media/commercial.5f5f9bbc.svg)

![[object Object] icon](/_next/static/media/condos.8a55189e.svg)

![[object Object] icon](/_next/static/media/newLaunches.e1f1ccfd.svg)

![[object Object] icon](/_next/static/media/agents.9f8252e2.svg)

![[object Object] icon](/_next/static/media/guides.f567fc08.svg)

![[object Object] icon](/_next/static/media/contactUs.a39ef3b7.svg)

![[object Object] icon](/_next/static/media/aboutUs.e47cbd6d.svg)

)

Shariah-Compliant Home Financing: How Malaysia Is Redefining Ethical Property Ownership

Key Takeaways

- Ethical Financing Model: Shariah-compliant home financing avoids interest and emphasizes fairness and asset-backed transactions.

- Malaysia’s Leadership: Malaysia is a global benchmark for Islamic finance innovation and regulation.

- Diverse Structures: Financing models include Murabahah, Ijarah, and Tawarruq to suit different needs.

- Ongoing Challenges: Issues like Shariah non-compliance income highlight the need for stronger governance.

- Growing Global Demand: Ethical and faith-based finance is expanding rapidly worldwide.

Introduction to Shariah-Compliant Home Financing

In 2026, Shariah-compliant home financing is no longer a niche concept—it has become a major force in global finance. As more buyers seek ethical ways to own property, Malaysia stands out as a leading example of how finance, religion, and innovation can align successfully.

This growing sector is driven by a commitment to transparency, fairness, and trust. However, challenges around compliance and authenticity continue to shape its evolution, making it a dynamic and closely watched space.

What Is Shariah-Compliant Home Financing?

Shariah-compliant home financing is built on Islamic principles that prohibit riba (interest) and promote shared risk and ethical transactions. Instead of lending money for profit, financial institutions structure deals around real assets and trade-based agreements1.

These financing models ensure that profit is earned through legitimate economic activity rather than speculative or exploitative practices, making them both religiously compliant and economically viable.

How Islamic Mortgages Actually Work

Islamic mortgages operate differently from conventional loans. Instead of charging interest, the bank participates in the property transaction—either by purchasing and reselling the asset or leasing it to the buyer over time2.

This structure ensures that financial returns are tied to real assets, reinforcing the principle that money alone should not generate profit.

)

Conceptual representation of asset-based property financing aligned with ethical and Shariah principles

Malaysia’s Leading Role in Islamic Home Financing

Malaysia has positioned itself as a global leader in Islamic finance, offering a wide range of Shariah-compliant home financing products. Banks continue to innovate with flexible structures that cater to diverse customer needs while maintaining strict compliance standards3.

This diversity reflects a mature financial ecosystem where ethical principles and modern banking coexist effectively.

The Hidden Challenge: Shariah Non-Compliance Income (SNCI)

Despite its growth, the industry faces challenges such as Shariah non-compliance income (SNCI), which arises when transactions unintentionally violate Islamic principles. This issue is particularly relevant in complex financing structures that involve multiple layers of transactions4.

To address this, regulators and financial institutions are strengthening governance, improving transparency, and enhancing compliance mechanisms.

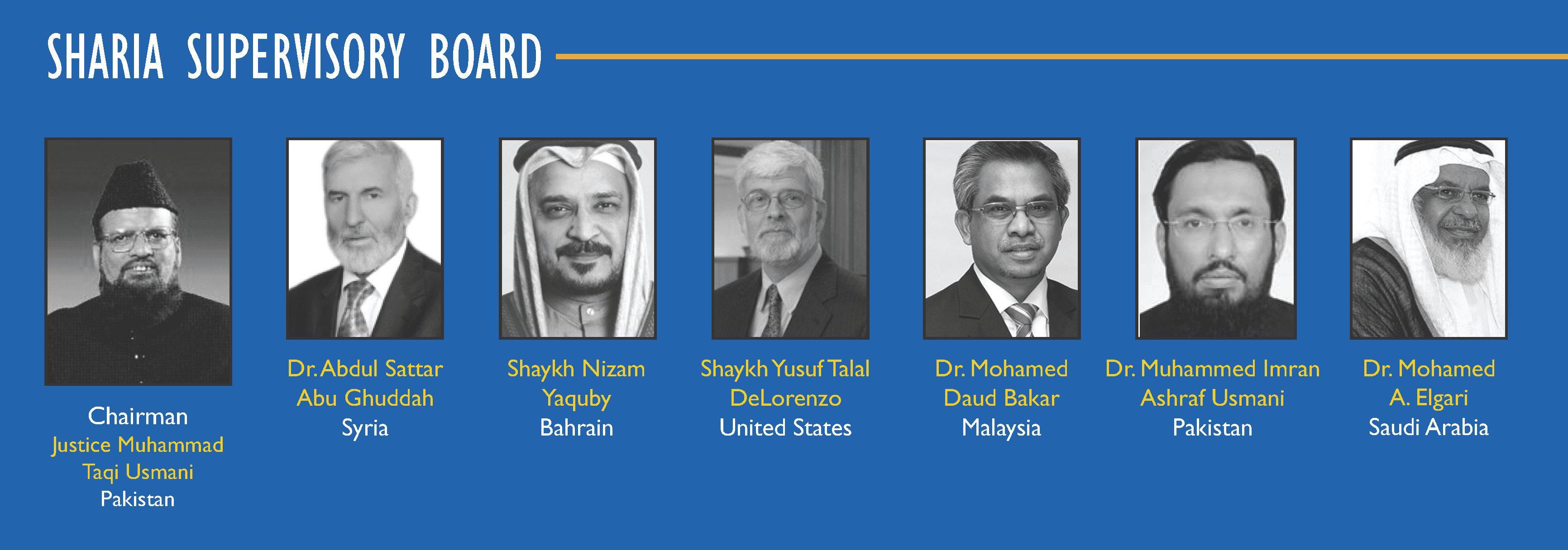

Why Shariah Boards Matter More Than Ever

Shariah boards play a crucial role in ensuring that financial products adhere to Islamic law. These expert panels review, monitor, and guide financial institutions to maintain ethical integrity across all transactions5.

{kind=link}

Their oversight is essential in building trust and ensuring that products are genuinely compliant, not just structurally adapted.

Islamic vs Conventional Mortgages

The core difference between Islamic and conventional mortgages lies in how profit is generated. Conventional loans rely on interest, while Islamic financing is based on trade, leasing, or partnership models that align with ethical principles6.

This distinction makes Islamic financing appealing not only for religious reasons but also for those seeking more transparent and fair financial systems.

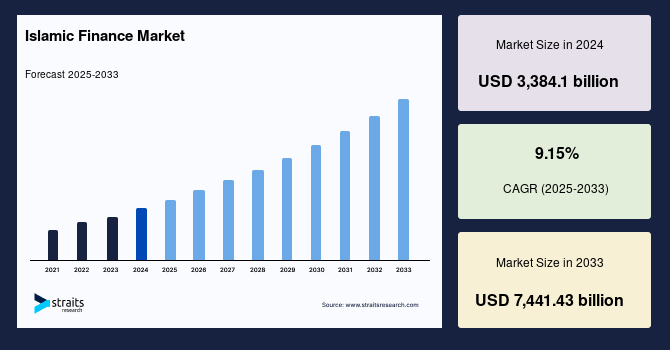

A Market on the Rise

The global Islamic finance market is expanding rapidly, with strong growth projections driven by increasing demand for ethical financial solutions. Malaysia continues to lead by setting high standards in regulation and innovation7.

{kind=link}

This growth highlights a broader shift toward values-based finance in modern economies.

Reforming for Trust, Justice, and Transparency

Ongoing reforms in Malaysia focus on strengthening trust and ensuring fairness across the Islamic home financing sector. Emphasis is placed on transparency, accountability, and aligning financial practices with core ethical values8.

These efforts aim to create a more robust and trustworthy system for future growth.

Why Consumer Education Is the Missing Piece

Understanding remains one of the biggest barriers to adoption. Many buyers find Islamic financing concepts complex, which highlights the need for accessible and clear educational resources9.

Improving awareness will help consumers make informed decisions and build confidence in the system.

The Bigger Picture: Ethical Finance for the Future

Shariah-compliant home financing represents more than a religious framework—it reflects a global shift toward ethical finance. By focusing on transparency, shared responsibility, and real economic activity, it offers a compelling alternative to conventional systems.

Malaysia’s approach demonstrates how innovation and ethical values can coexist to create a sustainable financial future.

Final Thoughts

Shariah-compliant home financing is entering a transformative phase, driven by demand, innovation, and reform. Malaysia remains at the forefront, shaping the future of ethical property ownership.

While challenges persist, the continued focus on trust, compliance, and education will determine how this sector evolves in the years ahead.

As global interest in ethical finance grows, this model is increasingly becoming a standard rather than an alternative.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional loans?

Answer: It avoids interest and instead uses asset-based transactions where profit is generated through trade, leasing, or partnerships.

Question: Is Islamic home financing only for Muslims?

Answer: No, it is open to anyone interested in ethical and interest-free financing solutions.

Question: Why is Malaysia considered a leader in Islamic finance?

Answer: Malaysia has strong regulations, innovative financial products, and well-established Shariah governance frameworks.

Disclaimer: The information is provided for general information only. JYMS Properties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.