![[object Object] icon](/_next/static/media/home.59b745c9.svg)

![[object Object] icon](/_next/static/media/buy.57cae078.svg)

![[object Object] icon](/_next/static/media/rent.2864d22a.svg)

![[object Object] icon](/_next/static/media/commercial.5f5f9bbc.svg)

![[object Object] icon](/_next/static/media/condos.8a55189e.svg)

![[object Object] icon](/_next/static/media/newLaunches.e1f1ccfd.svg)

![[object Object] icon](/_next/static/media/agents.9f8252e2.svg)

![[object Object] icon](/_next/static/media/guides.f567fc08.svg)

![[object Object] icon](/_next/static/media/contactUs.a39ef3b7.svg)

![[object Object] icon](/_next/static/media/aboutUs.e47cbd6d.svg)

)

Islamic Sharia-compliant Home Financing: A 2026 Guide to Ethical Homeownership

Key Takeaways

- Interest-Free Structure: Islamic financing avoids riba by using trade and partnership-based contracts.

- Ethical Foundations: Transactions emphasize fairness, shared risk, and real asset involvement.

- Growing Global Demand: Adoption is rising in regions like Malaysia, the Middle East, and Europe.

- Ongoing Challenges: Concerns remain about authenticity and similarity to conventional loans.

- Innovation Ahead: New models aim to improve transparency and align closer with Sharia principles.

Introduction to Islamic Home Financing

In 2026, conversations around Islamic Sharia-compliant home financing are gaining new attention as rising housing costs and financial awareness push more people to question whether homeownership can align with faith. This financing model operates under ethical principles that prohibit interest and promote fairness, shared responsibility, and real economic activity1.

Instead of lending money for profit, Islamic finance structures transactions around tangible assets and partnerships. This creates a system where financial gain is tied to real economic value rather than speculative interest-based earnings2.

What Is Islamic Sharia-compliant Home Financing?

Islamic home financing allows individuals to purchase property without engaging in interest-based loans. Financial institutions instead use structured agreements such as cost-plus sales or joint ownership models to facilitate homeownership while maintaining compliance with religious guidelines3.

These structures are grounded in core principles such as risk-sharing, asset-backed transactions, and avoidance of uncertainty. Together, they form a system that differs fundamentally from conventional mortgages while aiming to achieve similar practical outcomes.

How Does It Work? Simple Examples

Although it may appear complex at first, Islamic home financing is based on a few straightforward models that define how ownership and payments are structured between the buyer and the financial institution4.

- Murabaha: The bank purchases the property and sells it at a marked-up price payable in installments.

- Ijara: The bank leases the property to the buyer, who gradually acquires ownership over time.

- Musharakah: Both parties co-own the property, and the buyer progressively buys out the financier’s share.

These approaches ensure that transactions remain tied to real assets and shared responsibilities rather than purely financial lending.

Why It Matters for Muslims

For many Muslims, choosing Sharia-compliant financing is a deeply personal decision rooted in faith. Avoiding interest is considered a fundamental requirement, making financial decisions part of a broader ethical and spiritual lifestyle5.

This perspective transforms homeownership into more than just a financial milestone—it becomes an act aligned with religious values and long-term moral considerations.

The Growing Demand in 2026

The demand for Islamic home financing continues to grow globally, with strong adoption in Malaysia, the Middle East, and parts of Europe. Despite this growth, discussions around fairness and transparency highlight the need for ongoing improvements within the system6.

This expansion reflects both increased awareness and a desire for financial solutions that align with ethical and religious values.

The Big Challenge: Authenticity Concerns

A key issue in Islamic finance is whether modern products truly differ from conventional loans. Many consumers question why total repayment amounts can appear similar, raising concerns about whether these structures fully reflect Sharia principles7.

Academic research also highlights that customer perception plays a major role in shaping trust, particularly when financial products appear complex or insufficiently explained8.

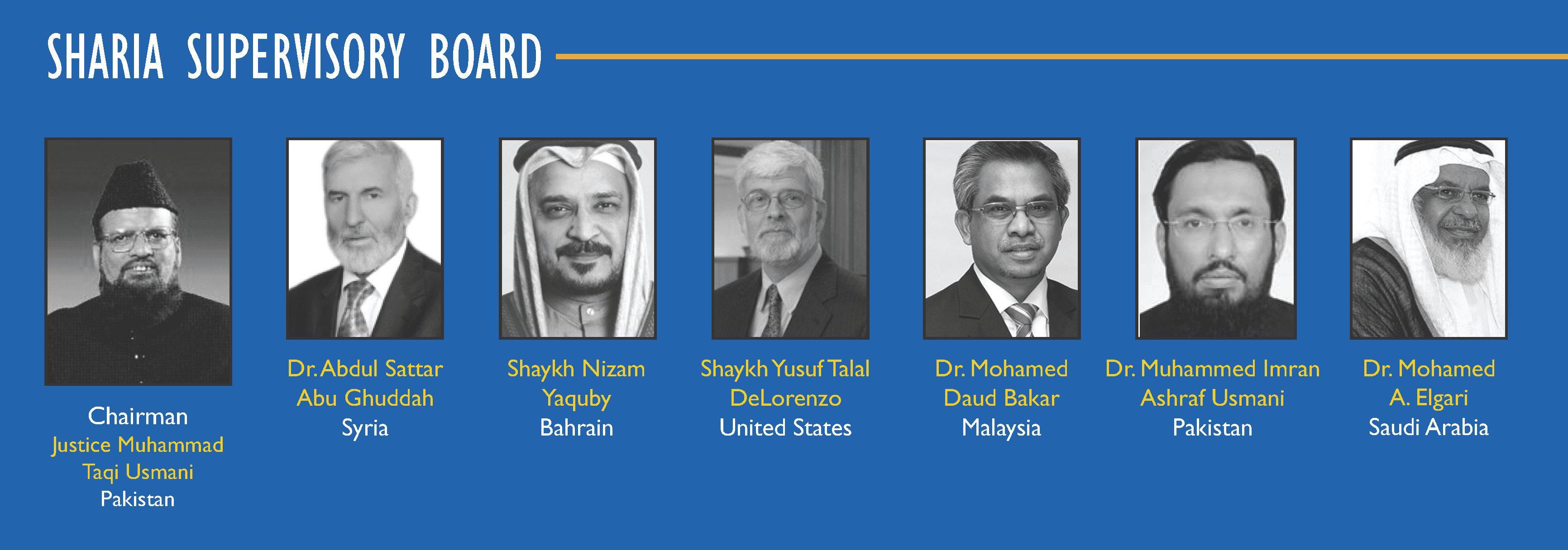

The Role of Shariah Boards

)

Organizational framework illustrating oversight by scholars ensuring ethical financial compliance

Shariah Boards play a central role in maintaining the integrity of Islamic financial institutions. These groups of scholars evaluate and approve financial products to ensure they meet religious and ethical standards9.

{kind=link}

By overseeing product development and compliance, these boards help build trust and ensure accountability across the industry.

Structural Issues: Tawarruq and SNCI

Debates around structures like Tawarruq and Shariah Non-compliance Income highlight the complexity of maintaining strict adherence to Islamic principles while meeting modern financial needs10.

These discussions show that Islamic finance is continuously evolving, with scholars and institutions working to refine practices and address emerging concerns.

Why Customer Awareness Matters

A major challenge today lies in customer understanding. Many buyers sign agreements without fully grasping the structure or implications of their financing contracts11.

Improving financial literacy can empower individuals to make informed decisions and strengthen confidence in Sharia-compliant systems.

Innovation in Islamic Home Financing

Innovation is shaping the future of Islamic finance, with new approaches such as using the House Price Index instead of traditional benchmarks to determine pricing structures12.

These developments aim to improve transparency and better align financial practices with real-world asset values.

Islamic vs Conventional Mortgages

The key difference between Islamic and conventional mortgages lies in how profit is generated. Islamic models are asset-based and partnership-driven, while conventional loans rely on interest payments13.

Despite these differences, the end financial outcomes can sometimes appear similar, making transparency and education essential.

The Trust Factor

Trust remains a cornerstone of Islamic home financing. Strengthening governance, improving communication, and enhancing transparency are all critical steps toward building long-term confidence in the system.

What Should Buyers Look For in 2026?

- Understand Contracts: Learn the differences between Murabaha, Ijara, and Musharakah.

- Check Profit Structure: Ask how payments and profit rates are calculated.

- Review Governance: Look into the institution’s Shariah Board.

- Read Carefully: Examine all terms and conditions before signing.

- Compare Options: Evaluate multiple providers before deciding.

The Future of Islamic Home Financing

The future of Islamic home financing looks promising, with continued advancements in transparency, regulation, and innovation. As the industry matures, it is expected to offer more refined and accessible solutions for ethical homeownership.

Final Thoughts

Islamic Sharia-compliant home financing in 2026 stands at an important turning point. It offers a meaningful alternative to conventional systems while continuing to address challenges related to trust and understanding.

With ongoing improvements in governance, innovation, and education, the system is steadily moving toward its goal of enabling ethical and faith-aligned homeownership.

Frequently Asked Questions

Question: What makes Islamic home financing different from conventional mortgages?

Answer: Islamic home financing avoids interest and instead uses asset-based or partnership models where profit is earned through trade or shared ownership.

Question: Is Islamic home financing more expensive than conventional loans?

Answer: The total cost can sometimes appear similar, but the structure differs significantly as it is based on ethical and asset-backed principles rather than interest.

Question: How can I verify if a financing product is truly Sharia-compliant?

Answer: You can review the institution’s Shariah Board, understand the contract structure, and seek clarification from qualified scholars or financial experts.

Disclaimer: The information is provided for general information only. JYMS Properties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.