![[object Object] icon](/_next/static/media/home.59b745c9.svg)

![[object Object] icon](/_next/static/media/buy.57cae078.svg)

![[object Object] icon](/_next/static/media/rent.2864d22a.svg)

![[object Object] icon](/_next/static/media/commercial.5f5f9bbc.svg)

![[object Object] icon](/_next/static/media/condos.8a55189e.svg)

![[object Object] icon](/_next/static/media/newLaunches.e1f1ccfd.svg)

![[object Object] icon](/_next/static/media/agents.9f8252e2.svg)

![[object Object] icon](/_next/static/media/guides.f567fc08.svg)

![[object Object] icon](/_next/static/media/contactUs.a39ef3b7.svg)

![[object Object] icon](/_next/static/media/aboutUs.e47cbd6d.svg)

)

Shariah-Compliant Home Financing: A Clear Guide to Ethical Homeownership in 2026

Key Takeaways

- Interest-Free Structure: Shariah-compliant financing avoids riba by using trade or leasing models instead of loans.

- Asset-Backed Transactions: Financing is tied to real property, ensuring ethical and transparent dealings.

- Malaysia Leads Innovation: The country remains a global benchmark for Islamic home financing models.

- Trust and Compliance Matter: Strong governance and Shariah oversight are critical for consumer confidence.

- Fintech is Transforming the Sector: Technology is improving transparency, speed, and accessibility.

What Is Shariah-Compliant Home Financing?

In 2026, Shariah-compliant home financing is gaining strong attention across global markets, especially in countries like Malaysia. It allows individuals to purchase homes without involving interest (riba), which is prohibited in Islam. Instead of lending money, financial institutions structure transactions around buying, selling, or leasing assets to ensure ethical compliance1.

In a conventional mortgage, borrowers repay a loan with interest over time. In contrast, Islamic financing involves the bank purchasing the property and then selling or leasing it to the buyer at an agreed profit, making the transaction asset-based and transparent.

For a broader understanding of Shariah-compliant structures like Musharakah and Murabahah, many modern guides explore how ethical homeownership is structured in practice2.

Key Differences: Islamic vs Conventional Mortgages

The difference between Islamic and conventional mortgages lies in structure and philosophy. Conventional loans rely on interest, while Shariah-compliant models are based on trade and shared risk, ensuring fairness and transparency in transactions.

- Conventional mortgage:

- You borrow money

- You pay interest

- The bank profits from interest

- Shariah-compliant financing:

- The bank buys the property

- You lease or purchase it

- Profit is pre-agreed

This asset-backed approach ensures that financing is tied to real economic activity and avoids speculative practices, aligning financial outcomes with ethical principles3.

Popular Islamic Home Financing Models in Malaysia

Malaysia stands as a global leader in Islamic finance, offering well-developed and widely adopted home financing models.

Commodity Murabahah

This model involves the bank purchasing a commodity and selling it to the customer at a marked-up price, payable in installments. It replaces interest with a cost-plus-profit structure widely used by financial institutions4.

Tawarruq Structure

Tawarruq involves multiple transactions to generate liquidity, but it has raised concerns regarding potential Shariah compliance issues such as unintended non-compliant income if not properly managed5.

The Trust Factor: Why Shariah Compliance Matters

As demand increases, trust has become a central issue. Some critics argue that certain Islamic financing products closely resemble conventional loans, prompting discussions on transparency and reform within the industry6.

Strengthening compliance frameworks and ensuring strict adherence to Islamic principles is essential to maintaining consumer confidence and long-term sustainability in the market7.

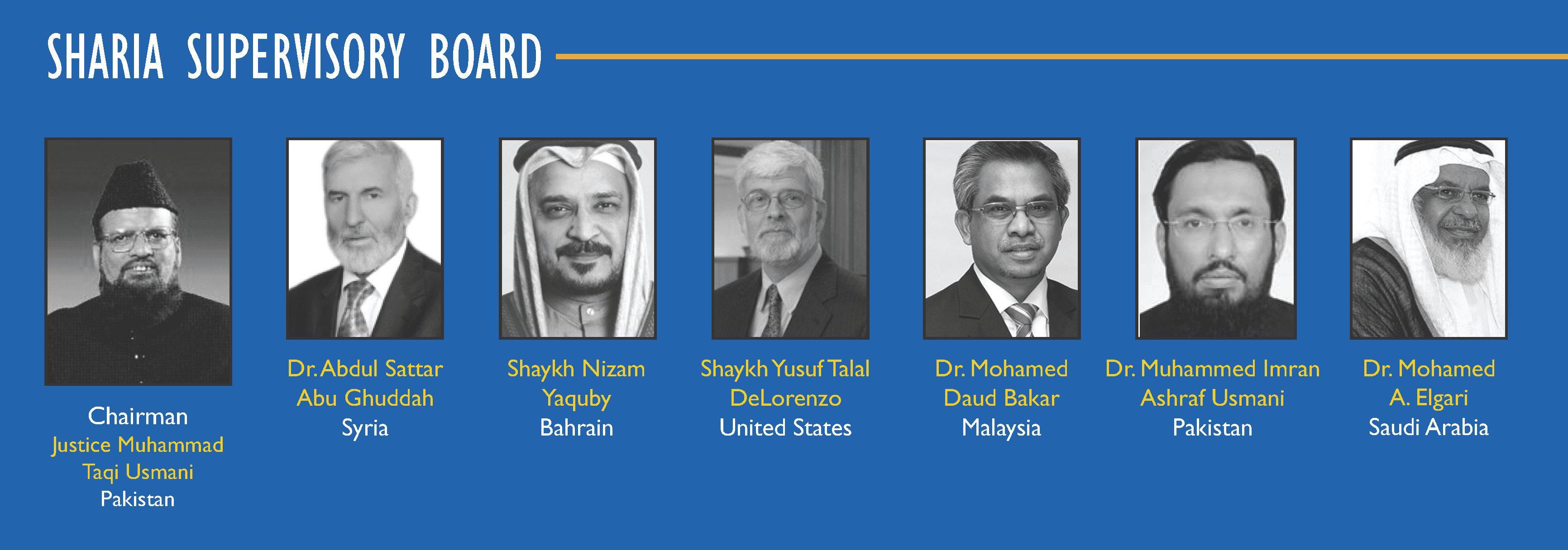

The Role of Shariah Boards

Shariah Boards play a vital role in ensuring that financial products comply with Islamic principles. These panels of scholars review, approve, and monitor financing structures, acting as ethical gatekeepers for the industry.

.webp)

Scholarly oversight ensuring ethical compliance in Islamic financial systems

Their governance ensures fairness, transparency, and adherence to the prohibition of interest, which are fundamental to maintaining trust in Islamic finance systems8.

{kind=link}

Why Consumer Awareness Is Still a Challenge

Despite growing adoption, many consumers still lack a clear understanding of how Islamic home financing works. Perception plays a major role, as uncertainty about structure and compliance can discourage potential buyers9.

Legal awareness also significantly impacts decision-making, with better-informed customers more likely to choose Shariah-compliant financing options10.

Real Products in the Market Today

Islamic home financing is widely available through major financial institutions, offering practical solutions tailored to modern homebuyers.

Products like Saadiq My Home-i provide flexible options aligned with Shariah principles, while innovations such as Smart Mortgage Home aim to enhance adaptability and user experience11.

These offerings reflect how banks are evolving to meet changing expectations while maintaining ethical standards12.

The Foundations of Islamic Finance in Housing

Islamic finance is built on principles such as risk-sharing, asset-backed transactions, and ethical investment. These foundations distinguish it from conventional systems and ensure that financial activities contribute to real economic value13.

Technology Is Changing the Game

In 2026, fintech is transforming Islamic finance by improving transparency, automating compliance checks, and simplifying complex processes. These advancements are making Shariah-compliant financing more accessible and efficient for a wider audience14.

{kind=link}

Challenges That Still Need Solving

Despite significant progress, several challenges remain, including perception issues, complexity of certain financing structures, lack of standardization, and regulatory gaps that require ongoing attention.

Why It Matters More Than Ever

For many homebuyers, Shariah-compliant financing represents more than a financial choice—it reflects a commitment to ethical living, fairness, and spiritual alignment in major life decisions.

The Future of Shariah-Compliant Home Financing

The future of Islamic home financing looks promising, with continued innovation, stronger governance, improved education, and integration of advanced technologies shaping a more transparent and trustworthy ecosystem.

Final Thoughts

Shariah-compliant home financing represents a meaningful shift in how people approach homeownership, combining ethical values with practical financial solutions. As the industry evolves, it continues to offer a viable and principled alternative to conventional systems.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional loans?

Answer: It avoids interest and instead uses trade-based or leasing structures where profit is agreed upfront and transactions are tied to real assets.

Question: Is Shariah-compliant financing only for Muslims?

Answer: No, it is open to anyone interested in ethical and interest-free financial solutions, regardless of religious background.

Question: Are Islamic home financing products truly interest-free?

Answer: Yes, they are structured to avoid interest, although they include profit margins agreed upon in advance through permissible trade-based contracts.

Disclaimer: The information is provided for general information only. JYMS Properties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.