![[object Object] icon](/_next/static/media/home.59b745c9.svg)

![[object Object] icon](/_next/static/media/buy.57cae078.svg)

![[object Object] icon](/_next/static/media/rent.2864d22a.svg)

![[object Object] icon](/_next/static/media/commercial.5f5f9bbc.svg)

![[object Object] icon](/_next/static/media/condos.8a55189e.svg)

![[object Object] icon](/_next/static/media/newLaunches.e1f1ccfd.svg)

![[object Object] icon](/_next/static/media/agents.9f8252e2.svg)

![[object Object] icon](/_next/static/media/guides.f567fc08.svg)

![[object Object] icon](/_next/static/media/contactUs.a39ef3b7.svg)

![[object Object] icon](/_next/static/media/aboutUs.e47cbd6d.svg)

)

Shariah-Compliant Home Financing: The Future of Ethical Property Ownership in 2026

Key Takeaways

- Ethical Financing Growth: Shariah-compliant home financing is becoming mainstream due to demand for transparent and fair financial systems.

- Interest-Free Principle: These models avoid interest and instead rely on asset-based transactions and shared risk.

- Diverse Financing Structures: Options like Murabahah, Musharakah, and Tawarruq provide flexible approaches to homeownership.

- Regulatory Evolution: Countries like Malaysia are refining frameworks to ensure authenticity and fairness.

- Global Expansion: Markets beyond traditional hubs are beginning to adopt Islamic financing solutions.

Introduction to Shariah-Compliant Home Financing

In 2026, Shariah-Compliant Home Financing is no longer a niche concept—it is rapidly becoming a mainstream option for homebuyers seeking ethical, transparent, and faith-based alternatives to traditional mortgages. Demand continues to grow across Southeast Asia as financial solutions align with Islamic principles while supporting modern housing needs1.

This transformation reflects a broader shift toward accountability, fairness, and shared responsibility in finance, with institutions innovating to meet both ethical expectations and practical affordability requirements.

What Is Shariah-Compliant Home Financing?

At its core, Shariah-compliant home financing is based on the principle that money cannot generate profit on its own, eliminating the use of interest and replacing it with asset-backed transactions and partnerships2.

Instead of issuing loans, financial institutions engage in buying, selling, or co-owning property with the buyer. This shifts the framework from debt-based financing to trade and shared ownership, fundamentally changing how risk and profit are distributed.

Why It’s Trending in 2026

The rapid growth of Islamic finance is driven by increasing demand for ethical financial systems, government backing, and expansion into new regions. Industry projections indicate strong global growth, with home financing emerging as a key segment in this expansion3.

{kind=link}

This rise is not solely religious but reflects a broader global interest in responsible and transparent financial practices.

How It Works: The Key Structures

Murabahah (Cost-Plus Sale)

This model involves the bank purchasing a property and reselling it to the buyer at a marked-up price, which is paid in installments. It ensures predictable payments while maintaining compliance with Islamic principles4.

Musharakah (Partnership Model)

In this structure, the bank and buyer jointly own the property, with the buyer gradually acquiring full ownership. It emphasizes genuine risk-sharing and aligns closely with Islamic financial ethics.

Tawarruq (Commodity-Based Financing)

This approach uses commodity transactions to create liquidity, though it has sparked debate regarding its compliance in practice, prompting calls for stricter oversight5.

Smart Islamic Mortgages

Modern offerings now combine flexibility and compliance, providing innovative solutions tailored to evolving buyer expectations6.

The Push for Reform: Malaysia Leads the Way

)

Principles of justice, transparency, and ethical finance shaping modern Islamic home financing reforms

Malaysia remains a leader in Islamic finance innovation, yet ongoing discussions highlight the need for reforms to ensure products genuinely reflect Shariah principles rather than merely replicating conventional structures7.

Scholars emphasize that improvements should focus on fairness, transparency, and true risk-sharing to strengthen trust and authenticity within the system8.

{kind=link}

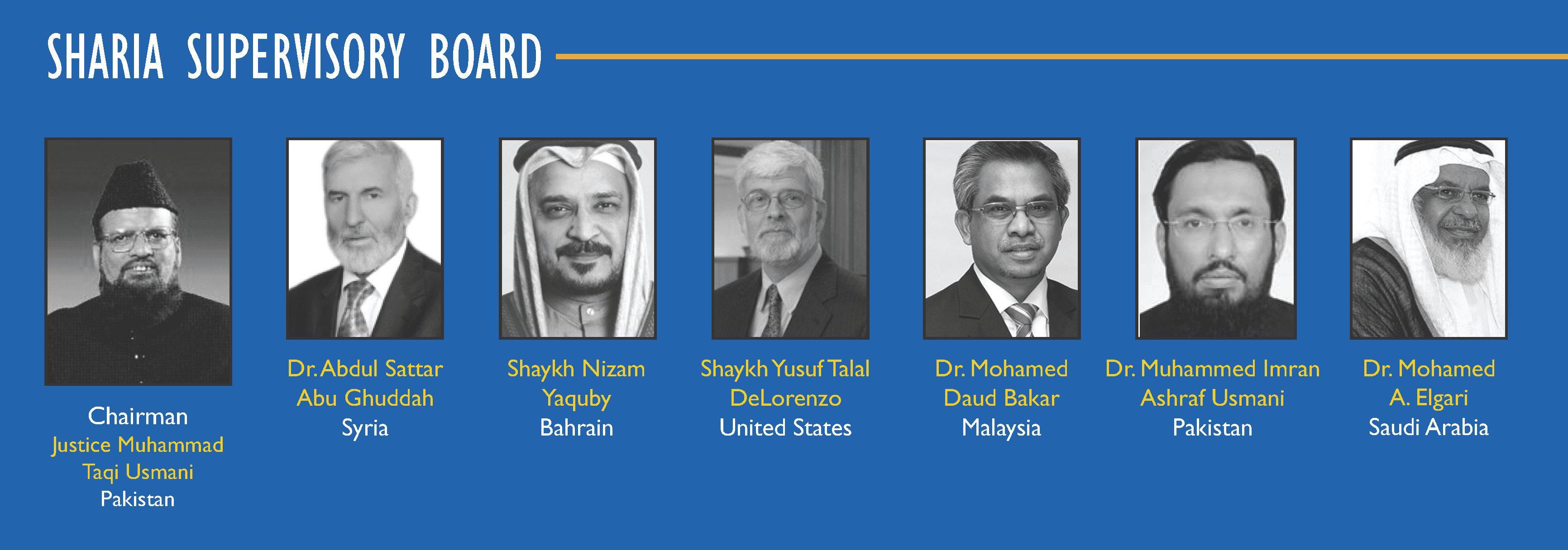

The Role of Shariah Boards

Shariah boards play a critical role in ensuring that financial products comply with Islamic law by reviewing structures, approving contracts, and monitoring operations for ongoing compliance9.

{kind=link}

Their presence provides assurance to buyers that financial arrangements adhere to ethical and religious standards.

Real-World Decisions: Islamic vs Conventional Loans

Homebuyers often weigh factors such as cost, flexibility, and transparency when choosing between Islamic and conventional financing, with discussions highlighting both advantages and trade-offs in real-world scenarios10.

While some choose based on religious values, others are drawn to the ethical and transparent framework offered by Shariah-compliant products.

Expanding Beyond Malaysia: Singapore Steps In

New markets are beginning to explore Shariah-compliant financing solutions, signaling broader adoption and increased global relevance as demand for ethical finance grows.

Buying a Home with Shariah Compliance

The home buying process remains familiar, but financing decisions require additional considerations such as contract structure, compliance approval, and ethical alignment.

Challenges Facing the Industry

- Complex Structures: Financing models can be harder to understand than conventional loans.

- Authenticity Issues: Some products face criticism for closely resembling traditional interest-based loans.

- Regulatory Gaps: Differences across countries create inconsistencies.

- Cost Perception: Misconceptions persist about higher costs.

The Ethical Edge: Why It Matters

Islamic finance emphasizes fairness, transparency, and real economic activity, offering an alternative approach that resonates beyond religious boundaries.

What Comes Next?

- Standardization: Greater consistency across global markets.

- Digital Innovation: Integration with fintech solutions.

- Transparency: Clearer contracts and pricing structures.

- Stronger Oversight: Enhanced regulatory frameworks.

Final Thoughts

Shariah-Compliant Home Financing in 2026 represents a growing shift toward ethical and responsible property ownership. As the industry evolves, balancing innovation with authenticity will be key to maintaining trust and long-term sustainability.

For homebuyers, it offers a meaningful path to ownership rooted in fairness and shared responsibility, reinforcing the idea that how a home is financed is just as important as the home itself.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional mortgages?

Answer: It avoids interest and instead uses asset-based transactions or partnerships, focusing on shared risk and ethical financial practices.

Question: Is Shariah-compliant financing more expensive?

Answer: Not necessarily. Costs vary depending on the structure and provider, and some options are competitive with conventional loans.

Question: Can non-Muslims apply for Shariah-compliant home financing?

Answer: Yes, these financing options are open to anyone interested in ethical and transparent financial solutions.

Disclaimer: The information is provided for general information only. JYMS Properties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.